Hello, in this particular article you will provide several interesting pictures of example of journal to ledger.html. We found many exciting and extraordinary example of journal to ledger.html pictures that can be tips, input and information intended for you. In addition to be able to the example of journal to ledger.html main picture, we also collect some other related images. Find typically the latest and best example of journal to ledger.html images here that many of us get selected from plenty of other images.

We all hope you can get actually looking for concerning example of journal to ledger.html here. There is usually a large selection involving interesting image ideas that will can provide information in order to you. You can get the pictures here regarding free and save these people to be used because reference material or employed as collection images with regard to personal use. Our imaginative team provides large dimensions images with high image resolution or HD.

We all hope you can get actually looking for concerning example of journal to ledger.html here. There is usually a large selection involving interesting image ideas that will can provide information in order to you. You can get the pictures here regarding free and save these people to be used because reference material or employed as collection images with regard to personal use. Our imaginative team provides large dimensions images with high image resolution or HD.

example of journal to ledger.html - To discover the image more plainly in this article, you are able to click on the preferred image to look at the photo in its original sizing or in full. A person can also see the example of journal to ledger.html image gallery that we all get prepared to locate the image you are interested in.

example of journal to ledger.html - To discover the image more plainly in this article, you are able to click on the preferred image to look at the photo in its original sizing or in full. A person can also see the example of journal to ledger.html image gallery that we all get prepared to locate the image you are interested in.

We all provide many pictures associated with example of journal to ledger.html because our site is targeted on articles or articles relevant to example of journal to ledger.html. Please check out our latest article upon the side if a person don't get the example of journal to ledger.html picture you are looking regarding. There are various keywords related in order to and relevant to example of journal to ledger.html below that you can surf our main page or even homepage.

We all provide many pictures associated with example of journal to ledger.html because our site is targeted on articles or articles relevant to example of journal to ledger.html. Please check out our latest article upon the side if a person don't get the example of journal to ledger.html picture you are looking regarding. There are various keywords related in order to and relevant to example of journal to ledger.html below that you can surf our main page or even homepage.

Hopefully you discover the image you happen to be looking for and all of us hope you want the example of journal to ledger.html images which can be here, therefore that maybe they may be a great inspiration or ideas throughout the future.

Hopefully you discover the image you happen to be looking for and all of us hope you want the example of journal to ledger.html images which can be here, therefore that maybe they may be a great inspiration or ideas throughout the future.

All example of journal to ledger.html images that we provide in this article are usually sourced from the net, so if you get images with copyright concerns, please send your record on the contact webpage. Likewise with problematic or perhaps damaged image links or perhaps images that don't seem, then you could report this also. We certainly have provided a type for you to fill in.

All example of journal to ledger.html images that we provide in this article are usually sourced from the net, so if you get images with copyright concerns, please send your record on the contact webpage. Likewise with problematic or perhaps damaged image links or perhaps images that don't seem, then you could report this also. We certainly have provided a type for you to fill in.

The pictures related to be able to example of journal to ledger.html in the following paragraphs, hopefully they will can be useful and will increase your knowledge. Appreciate you for making the effort to be able to visit our website and even read our articles. Cya ~.

The pictures related to be able to example of journal to ledger.html in the following paragraphs, hopefully they will can be useful and will increase your knowledge. Appreciate you for making the effort to be able to visit our website and even read our articles. Cya ~.

- Topic 4: Journal, Ledger") Q1walkthrough example (journal, ledger, TB) - Topic 4: Journal, Ledger

Q1walkthrough example (journal, ledger, TB) - Topic 4: Journal, Ledger

Bookkeeping Example of Business Transaction, Journal, Ledger, Report

Bookkeeping Example of Business Transaction, Journal, Ledger, Report

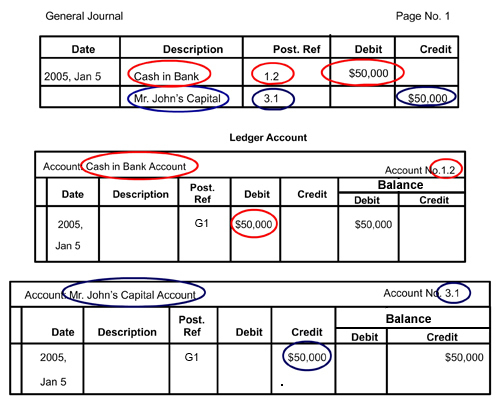

General Journal | Accounting Corner

General Journal | Accounting Corner

General Journal | Accounting Corner

General Journal | Accounting Corner

Journal | Ledger | Trial Balance Solution - CommerceLessonin

Journal | Ledger | Trial Balance Solution - CommerceLessonin

Bookkeeping Example of Business Transaction, Journal, Ledger, Report

Bookkeeping Example of Business Transaction, Journal, Ledger, Report

General Journal | Accounting Corner

General Journal | Accounting Corner

Neat 15 Transactions With Their Journal Entries Ledger Trial Balance

Neat 15 Transactions With Their Journal Entries Ledger Trial Balance

Accounting Examples - Journal, Ledger & TB | Download Free PDF

Accounting Examples - Journal, Ledger & TB | Download Free PDF

Journals and Ledgers in Bookkeeping - Zoho Books

Journals and Ledgers in Bookkeeping - Zoho Books

Sample General Ledger | Free Word Templates

Sample General Ledger | Free Word Templates

What is a Ledger in Accounting? Is There a Difference with a Journal

What is a Ledger in Accounting? Is There a Difference with a Journal

Accounting Ledger Book Example / general-ledger-sample-client-05-16

Accounting Ledger Book Example / general-ledger-sample-client-05-16

WHAT IS JOURNAL & LEDGER?

WHAT IS JOURNAL & LEDGER?